3.00% in a savings account is becoming more rare

There have only been a couple of savings account interest rate changes on our comparison chart over the past month. Neo Financial decreased its regular savings account interest rate from 3.00% to 2.50%, while Wealth One Bank of Canada actually increased its regular savings account and TFSA interest rate from 3.00% to 3.10%.

That still leaves PC Financial at the top of our chart for a regular savings account at 3.50%, while Wealth One Bank of Canada is the TFSA leader at 3.10%. All other non-promo rates are below 3.00%.

This has led to an increased number of discussions in our forum about what promotions are available.

Promos and longer-term GICs are looking more enticing

One of the promotions we track is at EQ Bank, where setting up an eligible direct deposit gets you 3.50%. This is down from 4.00% only a couple of weeks ago. Last month, we polled our readers about whether they have a direct deposit of at least $2,000, and 56% said no! Among the reasons given are that they are retired, self-employed, or unemployed.

Coast Capital is offering the highest promotional interest rate that we track, offering 5.00% on new deposits to a savings account if you become a new member by June 30.

Some GIC rates have been going up. 5-year rates are the highest (with Wealth One Bank of Canada at 4.00%), as was historically the case (prior to the past few years). The top 1-year (3.94%) and 2-year (3.97%) rates can currently be found at GIC brokers.

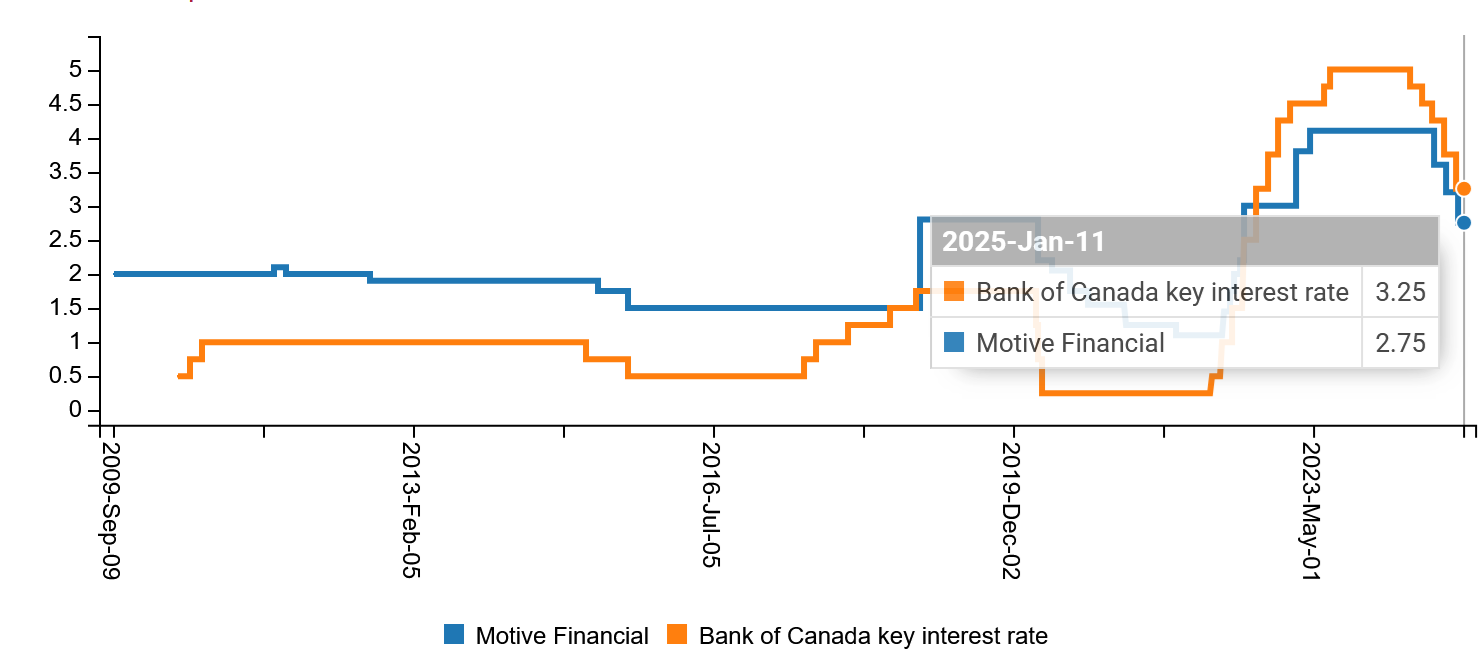

The Motive Financial brand is officially retiring

Last year’s announcement of National Bank’s takeover of Canadian Western Bank (which was Motive Financial’s parent company) affected a lot of savers, as Motive Financial has consistently been a savings account interest rate leader for over a decade.

National Bank emailed Motive Financial customers at the end of April to announce that the Motive Financial brand will be retired, and affected customers will be moved to accounts with National Bank. National Bank has promised “a similar interest rate”, although our forum users are skeptical about how long that will last, and assessing what to do next.