You have likely seen gold in one form or another. Gold can be jewellery, a luxury accessory, a fine dining flex, or the classic safe haven / hedge asset that investors gravitate towards when markets become a little too volatile. Gold as an asset and as a commodity has long carried a reputation for holding value and being considered the “gold standard”, which is why it continues to show up in conversations about diversification, inflation, and long-term investing. It is also one of those rare things that manages to be both serious and meme-worthy, whether it is associated with wealth, tradition, or a certain unforgettable Austin Powers reference to “Goldmember”.

So, what exactly is gold, and why do people buy it? Is it worth adding to a portfolio and holding onto? All these topics and more will be discussed in this two-part series as gold is broken down as an investment opportunity.

Understanding the basics of gold: a quick jump through time

Before being able to dive into the basic foundations of gold and its modern-day use cases, it is important to have the historical and cultural understanding of gold, and what led to its rise in popularity.

Gold has been traced as far back as ancient Mesopotamia around ~4000 BCE. Ancient civilizations used it for jewellery, religious artifacts, and symbols which were representative of divine power and wealth. Those who held gold were quickly considered powerful and wealthy, often seen as having divine status, as wealth was closely tied to both power and religious clout. Over time, gold began to outshine other metals like silver, bronze, and copper, which were heavily used during the Bronze Age for tools, weapons, and as early coinages. Part of the reason for gold becoming adopted and being highly sought after was simply because of its natural scarcity. Its high malleability also made it easier to shape without breaking or damaging. These traits continued forward with its association and characteristics of wealth and status until ~600 BCE when it replaced the legacy bartering system and became the official coinage for trade. And the rest, as they say, is history — and what we now know as the gold standard today, at least from a benchmark perspective.

What is the “gold standard”?

The “gold standard” was a monetary system where a country’s currency value was directly linked to a specific amount of gold. Essentially, the higher the gold reserve, the stronger the currency was. No major countries are tied or pegged to the gold standard anymore (since the USA essentially ended it in the 1970s). Today, the gold standard is commonly known as a metaphor for a benchmark representing the best-in-class to be used in comparisons.

What are the types of gold to invest in?

There are several ways to invest in gold, but they generally fall into two buckets: physical gold and paper gold. Physical gold includes bullion, bars, coins, and jewellery, while paper gold includes exchange-traded funds (ETFs), mutual funds, futures and forward contracts, and mining stocks. Each asset class has its own unique set of risks and benefits.

Physical gold

| Gold bullion |

Bullion refers to high-purity gold, typically in the form of bars or investment-grade coins, and its price is generally driven by the current spot price of gold (the live market price at which gold trades) plus any dealer markup, fabrication costs, and handling fees. |

| Gold bars |

A type of bullion, best for investors who want direct exposure to gold content, often with lower premiums than smaller retail products. Price is dictated based on the spot price of a single Oz of gold plus associated retailer fees. |

| Gold coins |

A type of bullion, gold coins are usually minted by governments or recognized refineries, and while their value is still closely tied to gold’s spot price, they often carry a higher premium than bars because of minting, collectability, and retail costs. They are often more liquid than bars, making them easier for re-sale. |

| Gold jewellery |

Gold jewellery is physical gold in the sense that it contains real gold that you can hold, but it is not typically considered investment-grade physical gold because premiums, craftsmanship, and resale discounts can reduce value. It is ideal for collectors or those who want something wearable with some gold content, but not for pure investing. |

Paper gold

| Gold ETFs and mutual funds |

Shares, funds, or trust units that track the price of gold rather than the metal itself. The price is usually tied to the spot market with fund fees and other product costs layered into the NAV (Net Asset Value of the investment). Best for investors who want exposure to the gold price without storing physical metal and want high liquidity assets. |

| Gold mining companies |

Shares of companies involved in exploring, mining, refining, or producing gold. Their value is influenced by the gold price, but also by the company’s performance, production costs, debt, management, and broader market conditions. Best for investors who want indirect exposure to gold with the potential for higher upside, but also higher volatility than physical gold or gold funds. |

| Gold futures |

Futures contracts that give investors exposure to the future price of gold rather than the metal itself. Their value is tied to the spot market and contract price. It can involve leverage, margin requirements, and contract rollover costs. Best for advanced investors who want tactical gold exposure and high liquidity, but can tolerate greater risk as leverage can drastically increase both gains and losses. |

Paper vs physical gold as an investment

When considering whether to buy gold, investors should be clear about what they are trying to achieve and how much risk they are comfortable taking on. For example, beginners may want to consider physical gold, as it is traditionally a relatively risk-off allocation (lower risk than paper gold and many other non-gold investments, as its price is impacted by the spot price of gold and in the case of jewellery, rarity). As a result, physical gold can offer direct exposure and diversification for investors.

By contrast, gold mining companies have additional risks such as management performance, property issues, legal risk, and even the possibility of mining nationalization. In that sense, mining stocks are more of a risk-on (higher risk at least compared to physical gold) way to gain exposure to gold, but can come with higher upside potential as their share price is impacted by more than just the spot price of gold. Gold funds, ETFs, and futures offer a variety of risks but have higher liquidity ratios and can be correlated to the spot price of gold or can leverage derivatives to increase upside potential. Of course, with higher upside potential there is also greater downside potential.

So rather than treating all gold investments the same, investors should think of them as different opportunities within the same space that have varying degrees of risk, liquidity, and upside potential.

Should I buy gold?

Whether or not you should buy gold depends on your goals, time horizon, and risk tolerance. Gold can be useful if you are looking for added diversification, a hedge against uncertainty, or exposure to a hard asset. However, gold is not designed to be a high-growth investment.

Historically, its performance is under 10% (annualized since 1916) and has had periods of extended stagnation. Recent years have experienced higher annualized returns due to heightened uncertainty and geopolitical tensions, sending the underlying asset to historic highs, hitting almost $5,600 USD an ounce in January 2026. However, because gold does not generate earnings, dividends, or cash flow, it is often not relied on as the primary growth engine for a portfolio and is generally a sleeve within a broader diversified portfolio.

When considering whether to buy gold or not, investors should consider if a specific type of gold exposure (the type of gold) fits or meets the role in their portfolio or life prior to investing, especially when nearing historic valuations.

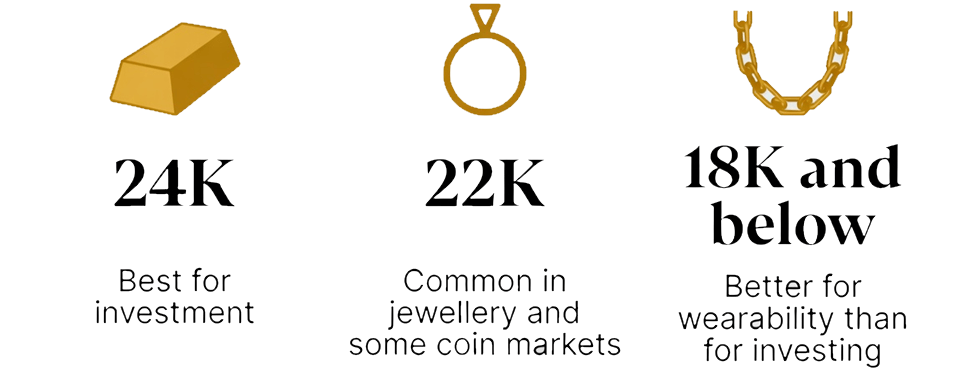

Karat gold, and what is its purpose?

Like other hard assets, gold has a valuation of purity that is known as “karat”. Gold purity or “karat” is valued out of 24 and it denotes the ratio of pure gold to base metals and alloys. The higher the karat, the higher the purity, and thus higher the value. At the same time, the lower the karat value, the higher alloy content, and thus generally lower value. For example, 24K or 24 karat gold is around 99-100% pure gold, which implies that the value of the item would be higher relative to the spot price of gold. A lower karat gold such as 18 karat, has around 75% gold, and its value would then be lower in contrast to 24 karat due to having a higher alloy content. What is important to note is that the karat level also impacts the end use. Lower karats, such as 22K, 18K, 14K, or 10K, are ideal for jewellery as they are more durable due to having higher alloy content; but it also means you are getting less gold per gram, so the value is less. If the goal is purely investment-based, then higher karat content is the direction. If the goal is more practical or jewellery based, then lower karat content is the direction.

How to verify the authenticity and purity of physical gold?

Before buying gold, it is important to verify both its authenticity and purity. The easiest way is to check for official stamps, mint markings, karat markings, assay certificates, and serial numbers where applicable. These steps are often easy to conduct, especially when buying gold from established and reliable places that are transparent with their offering. Organizations like major banks, recognized bullion dealers, governments, and retail stores like Walmart and Costco will have all these details available (and often on display). These establishments are also recommended for purchasing physical gold items vs online stores, secondary markets, or private sellers. This is due to their transparency, historical backings / established reputations, and clear return policies. An added benefit is that most established retailers will have secured delivery and proper storage for the precious metals.

| Aspect |

What to check / do |

Why it matters |

| Primary verification |

- Official stamps

- Karat markings / mint markings

- Serial numbers

- Assay certificates

|

Confirms purity and authenticity |

| Recommended purchase locations |

- Major banks

- Recognized bullion dealers

- Government mints/websites

- Trusted retailers (e.g. Walmart, Costco)

|

High transparency, clear policies, secure delivery |

| Best practices |

- Buy from reputable sellers

- Request original packaging & certification

- Check against recognized mint/refinery standards

|

Reduces risk of counterfeit or low-quality gold |

| For higher-value purchases |

- Use professional testing (jeweller, bullion dealer, or assay expert)

|

Extra assurance on large investments |

| Red flags |

- Deals that seem too good to be true, especially on secondary markets or private sellers

|

High risk of fraud or substandard product |

What are the risks of investing in gold?

Just like any investment, gold comes with its own unique set of risks. While gold can help diversify a portfolio and act as a hedge during periods of uncertainty, it is not entirely risk-free.

For example, the price of gold can fluctuate significantly based on market conditions, investor sentiment, interest rates, inflation expectations, and global economic events, sometimes even market volatility can play a role. If the market price of gold declines, the value of both physical and paper gold investments can decline as well.

As previously discussed, physical gold comes with liquidity and storage considerations. Unlike stocks or ETFs that can typically be bought and sold quickly on an exchange, selling physical gold can sometimes take longer depending on the type of asset and market demand. In certain situations, investors may need to sell through dealers, secondary markets, or private buyers, which can impact pricing and liquidity. Physical gold may also require secure storage and insurance, both of which can increase the overall cost of holding the investment. The value of physical gold can also vary depending on the form of the asset. For example, bullion products are generally tied closely to the spot price of gold, while collectibles may derive additional value from rarity, condition, historical significance, or brand recognition.

Paper gold investments, such as ETFs, mutual funds, and futures contracts, introduce a different set of risks. In addition to market risk, investors may also face product risk depending on how the investment is structured. For example, some gold ETFs and mutual funds may not hold physical gold directly and instead gain exposure through mining equities, futures contracts, derivatives, or other financial instruments. This can cause the investment’s performance to differ from the actual movement of physical gold. Additionally, because it is a paper gold investment, liquidity constraints can play a role too, which is why some ETFs or mutual funds may be delisted due to a lack of money-in-flow (not enough investment in the fund, and low liquidity so it is terminated).

More complex gold products introduce counterparty risk. This risk is generally associated with investments that rely on futures, swaps, derivatives, or contractual agreements between financial institutions rather than direct ownership of physical gold. Counterparty risk is where the other party in the transaction defaults on the contract before settlement, causing the value to decline or when an investor is trying to convert the paper asset into the underlying physical assets, but the physical asset is not delivered. In some cases, this could impact the value, settlement, or redemption of the investment. Complex products can be beneficial for experienced investors or those working directly with an investment professional.

So, is it better to buy gold coins, bars, or jewellery as an investment?

This comes down to personal preference but also an investor’s goals and intended use. Gold bars are often preferred by investors looking for lower premiums and direct exposure to the spot price of gold. Gold coins can offer better liquidity, recognizability, and collectability, but may come with slightly higher premiums. Jewellery, watches, and collectible pieces can sometimes generate strong returns due to brand value, rarity, and demand, but they can also be significantly harder to value and resell. For investors focused purely on gold exposure, bullion bars and investment-grade coins are generally an easier option.

Summary: how to invest in gold (basics about physical vs paper)

This is where many beginners get tripped up, because “owning gold” can mean very different things. Physical gold means you actually hold the metal in the form of bars or coins. Paper gold usually means gold ETFs, gold funds, mining stocks, or other financial instruments tied to the metal’s price.

Physical gold gives you direct ownership, but it also means dealing with storage, insurance, and security. It can also be less convenient to sell quickly if you need cash fast. Paper gold is easier to trade, simpler to buy in a brokerage account, and often cheaper to store, but it can introduce different risks because you do not personally hold the metal.

In plain English:

- Physical gold is better for people who want tangible ownership.

- Paper gold is better for people who want convenience and liquidity.

Stay tuned

If you enjoyed this introductory edition to the wonderful world of gold and its investment opportunities, stay tuned for part two of the series as we explore the technicals related to gold: the factors that impact the price of gold, tax implications, market drivers, and more!

Disclaimers

This article is independently written and not sponsored by any financial institution. The views expressed are solely those of the author(s) based on their research and analysis. The content is for informational purposes only and should not be considered financial advice. Always consult a qualified financial professional before making investment decisions. Reading this article does not create a professional relationship with the author(s) or affiliated organizations. It is not a substitute for personalized financial guidance.

Investing involves risks, including potential loss of principal. Readers are solely responsible for their investment decisions. Past performance does not guarantee future results. Historical or projected returns may not reflect actual future performance. The use of information in this article is at the reader’s own risk. The author and publisher are not responsible for any errors, omissions, or resulting losses/damages.