Credit Verify offers a free Canadian credit score and a $1 credit report. We do not recommend using them.

Automatic monthly charges

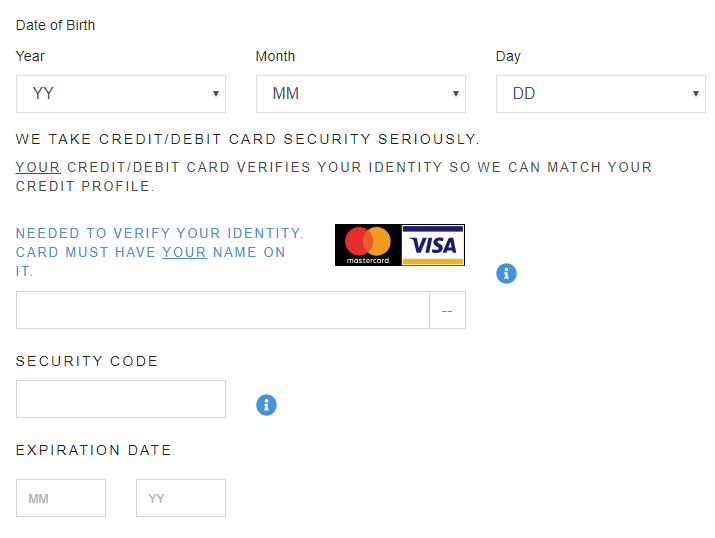

During the sign-up process, Credit Verify will ask you for your credit card, noting that it is required in order to verify your identity:

The main reason for Credit Verify to get your credit card is in order to charge your credit card a monthly fee (currently $29.95) after 7 days. Compare this against similar Canadian services such as Borrowell, which do not require you to supply your credit card information. You cannot cancel your Credit Verify account online or via email.

You will find a “Cancel” button in the online interface, but it will only lead to a message telling you to send a snail mail or to call them. Their mailing address was previously a US virtual mail service in California, and is now a co-working space in Squamish, BC. If you call their number to cancel, you will be subject to a hold that could be somewhere between 20 minutes and a few hours. You will then be subject to a spiel on the merits of the service, including the ability to correct errors in your credit report, and the reward that they give you each month. However, you will be able to cancel your account.

Credit Verify will not refund a charge they have already made on your credit card.

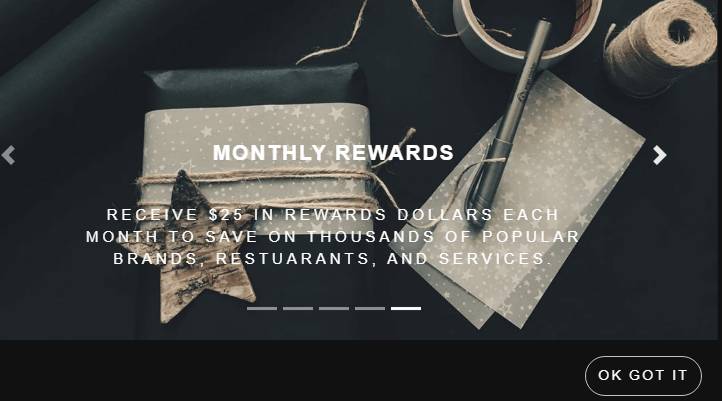

$25 “reward” each month

Credit Verify advertises the following as a feature of your account:

“You’ll receive $25 in Reward Dollars EACH month you’re a Credit Verify Premium member. Use your rewards however you’d like. Save on popular brands like Kate Spade, Michael Kors, Nike, Lacoste, or Under Armour. Get access to great local deals at the salon, dry-cleaning, car washes, movie tickets or golfing. Or you can save at popular restaurants like TGI Friday’s, Dunkin’ Donuts, McDonald’s, Subway and thousands more.”

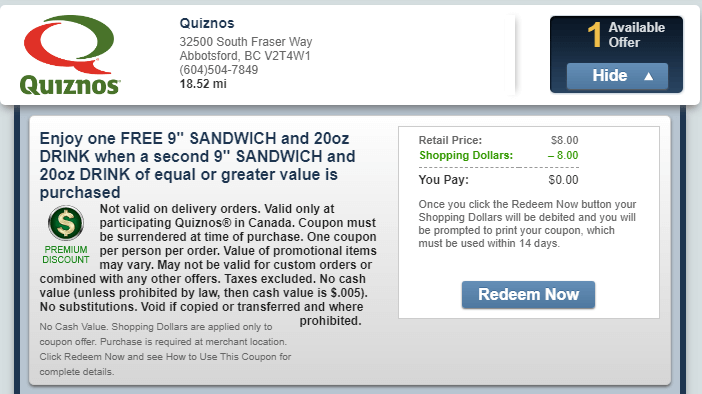

The monthly $25 reward they promote is no better than coupons you might get for free in the mail.

For example, buy a sandwich and drink and get another sandwich and drink free. Or, get a free drink if you purchase a burger, except you had to use your reward to get the coupon in the first place — and you still have to purchase the burger. We tested some hotel bookings through their travel discounts area, and found their prices to be more expensive than booking through the hotel’s own website.

Professional web presence?

Credit Verify is owned by a US company Credique LLC, whose mailing address is the same virtual mail service that used to be posted on Credit Verify’s website.

There are several typos on Credit Verify’s website, which have been there for months:

It is also telling that the social media icons in the footer of their website do not have links attached to them.

Other reviews

Be careful if you read a positive review of Credit Verify — scrutinize whether you can tell if the reviewer has actually used the service or is an affiliate of the service (and thus has affiliate links in their review).

Here are some links to other reviews of Credit Verify: