2.00% is a hot deal

You’re more likely to be earning closer to 1.00% than 2.00% on your savings right now. Such is the reality for Canadian savers, where 2% is a hot deal; here are a few examples:

- A new, non-registered Manulife Bank Advantage Account will get you 2.00% for 4 months

- motusbank is offering 2.40% in a new TFSA or RRSP savings account for 4 months if opened before June 30, 2021. Keep in mind that they have a $50 transfer-out fee for registered accounts.

- EQ Bank’s 2.30% TFSA and RRSP interest rate ends on May 26, but you can lock in a 2.30% 3-month TFSA or RRSP GIC before then

- Tangerine Bank has a promotional 2.10% savings account interest rate for the first 5 months if you also open a chequing account, plus a $150 bonus for setting up payroll direct deposit with the promo code “EARNMORE”

- Our GIC comparison chart features Oaken Financial and EQ Bank with 2.10% 5-year GICs, and LBC Digital with a 2.00% 5-year GIC

- Steinbach Credit Union has a special 2.00% 5-year GIC as well, as listed on our promotions page

- Toronto-based GIC broker GICWealth has a 2.15% 5-year GIC

It’s been another month full of interest rate drops on our savings account comparison chart at Oaken Financial (from 1.25% to 1.15%), Peoples Trust (from 1.20% to 1.15%), Wealth One Bank of Canada (from 1.50% to 1.25% on its regular savings account only), and Alterna Bank (from 1.10% to 1.00%). Neo Financial is about to decrease its regular savings account interest rate from 1.55% to 1.30% on Monday, May 17, leaving Canadian Tire Bank as the unmatched leader for both regular savings and TFSA accounts at 1.55%. Bridgewater Bank currently holds the second spot for a regular savings account at 1.45%, while Wealth One Bank of Canada holds the second spot for a TFSA at 1.50%.

Every account has its quirks: firsthand account reviews

Are you doing some spring cleaning on your bank accounts or potentially opening new ones? Our website community has been busy trying out new accounts and sharing experiences.

Top rate leader Wealth One Bank of Canada has a comprehensive set of account features on its chequing account, although its bill payments database could apparently use some work.

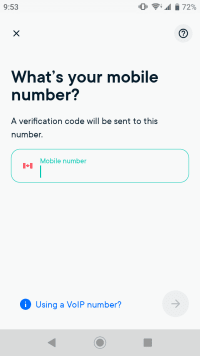

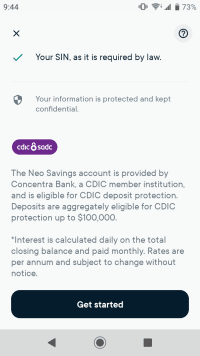

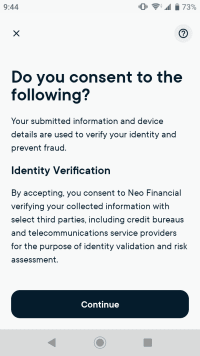

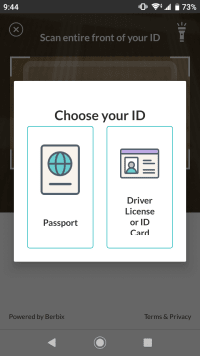

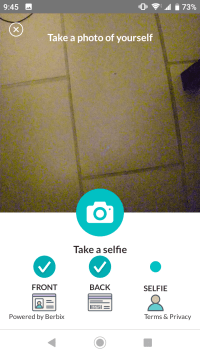

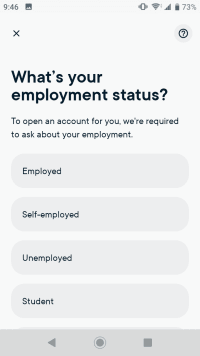

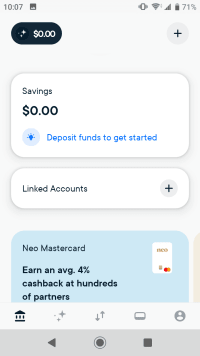

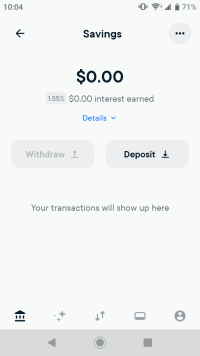

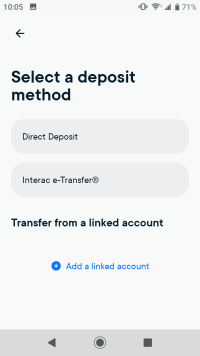

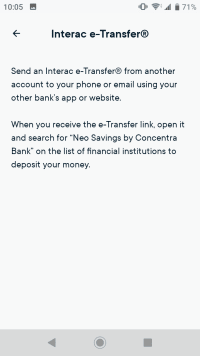

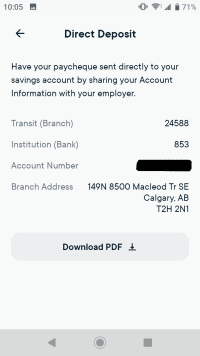

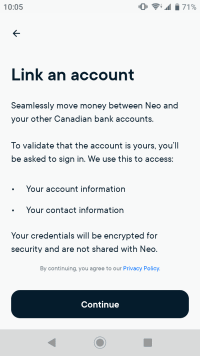

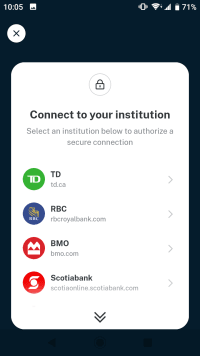

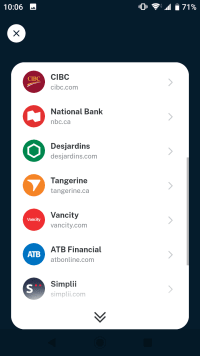

Neo Financial’s savings account interest rate is enticing (although less so with its impending decrease), but if you’re not quite sure about the new kid on the block, we’ve got the entire account opening process documented with screenshots, including how to link external accounts.

Several of the big banks have sign-up bonuses on their chequing accounts right now, but none of them support linking external accounts for “me to me” electronic funds transfers. Free Interac e-Transfers and cheques might still be good enough, and you can still link to the big bank accounts and initiate electronic funds transfers from many of the accounts listed on our website.

Spring reading

- An ode to GICs

- A discussion on how to ensure that your spouse can access your GICs if you die

- EQ Bank US dollar accounts are coming soon

Our top cash back offers

A few of the offers currently available on our cash back site include: