In a previous article, I reviewed some electronic options for paying your suppliers. One major disadvantage with most electronic payment options like wires and Interac e-Transfers is that they are not fully integrated into other software (such as a company’s bookkeeping software). Another disadvantage is that these options require a business owner to really trust someone to have full banking access, or to perform all the payment tasks herself. This translates to more administrative work, as opposed to running the actual business.

In today’s world of fintech, these disadvantages can be easily overcome. In this article, I (as a professional accountant) describe two popular options I have used to increase the efficiency of the accounts payable cycle: Plooto and RBC PayEdge. Plooto is an independent fintech startup which has been operating since 2015. RBC PayEdge used to be called WayPay Inc. It was also a startup but was acquired by Royal Bank of Canada (RBC) in mid-2019. The app’s functionality has not changed.

A better workflow

Both Plooto and RBC PayEdge are services that act as intermediaries between your books, your bank, and your recipient, and allow you to process payments in a secure and flexible way. The steps are roughly as follows:

- Supplier invoice arrives.

- Invoice is entered into the accounting system.

- This can be done manually by yourself or your bookkeeper. Or better yet, automate!

- Accounting system syncs with payment service.

- This is optional.

- Outstanding payables reviewed and submitted for review.

- Can be done by you or your bookkeeper.

- Payment service sends email to reviewer to notify them of pending payment.

- This is optional.

- Reviewer submits payment for processing.

- Payment service sends emails to both sender and recipient.

- When payment is approved, and also when it’s deposited in the recipient’s bank, so two emails in total for each person.

- Payment service syncs with accounting software to mark payment as complete.

- This is optional

Side note: You might ask, what about the accounts receivable cycle? That’s a bit different and I will touch on it later on.

Getting started

Set up: Connection to your bank

If you’ve ever used PayPal, you will be familiar with the process of connecting your bank account to an outside service. Plooto and RBC PayEdge both verify your identity (note, it must be a business) and there are procedures to follow to connect your bank account. The process takes several business days. There can be separate forms to fill out for domestic and foreign currency transactions.

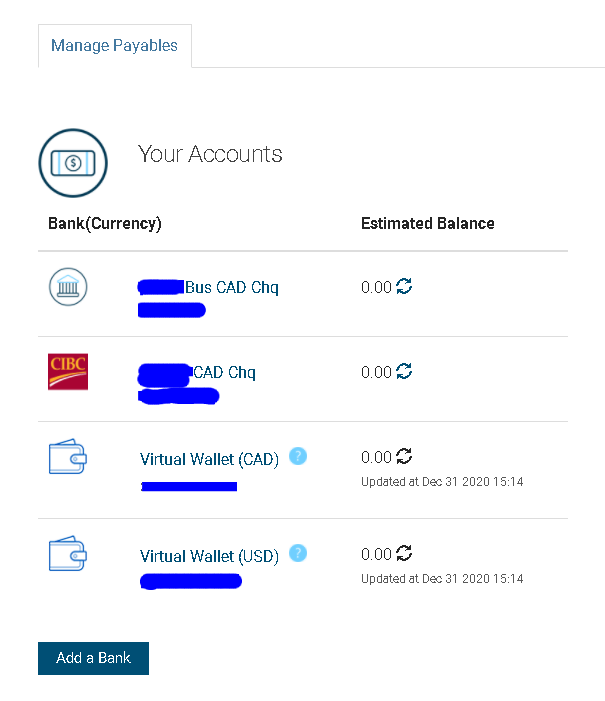

Here is an image of the RBC PayEdge bank accounts view:

Set up: Connection to your accounting software

Both solutions connect to popular cloud accounting software. I’ve had success with both QuickBooks Online (QBO) and Xero. As soon as a new invoice appears in QBO, it syncs with Plooto or RBC PayEdge, including attachments (such as a PDF copy of the invoice). When the payment clears, QBO is updated automatically.

Integration greatly reduces the chance of human error (data entry mistakes), and saves time.

Here is what a tax instalment payment looks like on the QBO banking page:

Tiers of approval

For most of my clients, I do not have payment approval rights. This means I can set up a payment and submit it, but my client makes the final approval. My client receives a notification via email and can approve the payment electronically from anywhere in the world as long as there is internet access.

For a larger operation, you can set up multiple approvers (similar to “dual signature” on cheques), and approval limits (“Manager James can approve up to $5,000 per payment”).

You need the recipient’s bank information

But, you only need it once. When a new invoice arrives, I send an email to the vendor on behalf of my client asking for a void cheque. I then enter the bank information into Plooto or RBC PayEdge. Clearly in this case there is trust between my client and myself, as this is sensitive information. Alternatively, a client can restrict staff to not be able to enter or adjust bank information.

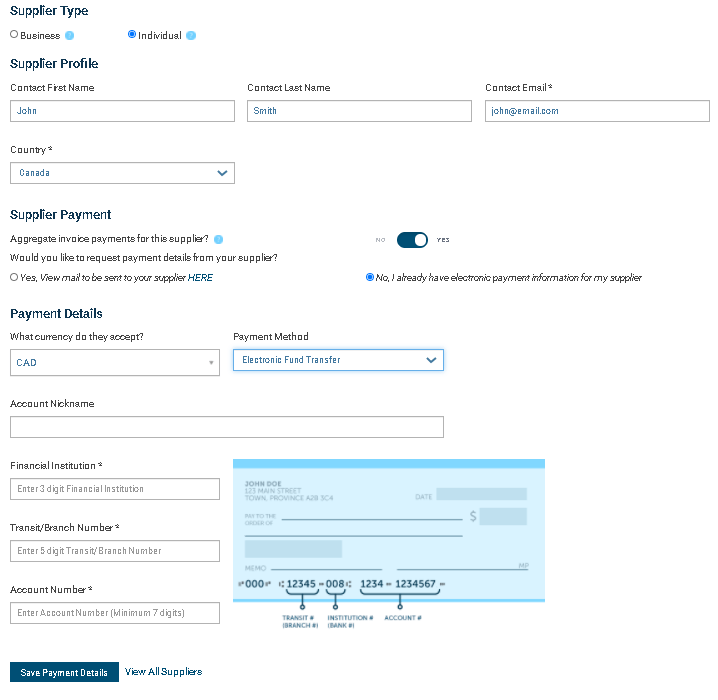

Here is an example of the supplier setup screen from RBC PayEdge:

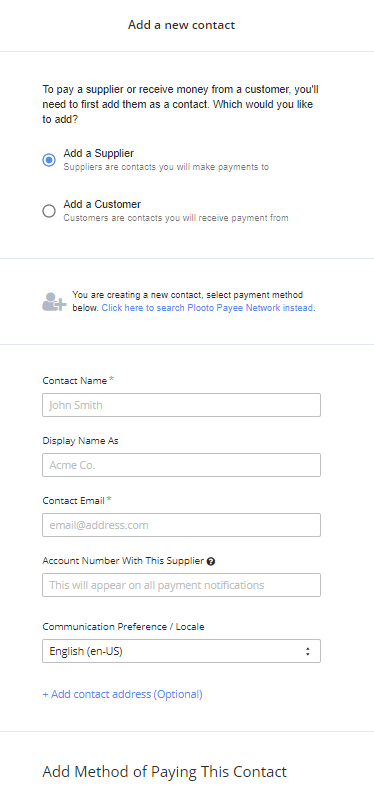

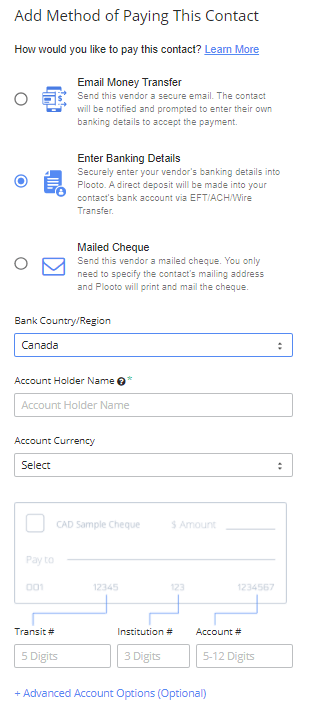

Here is the equivalent screen with Plooto:

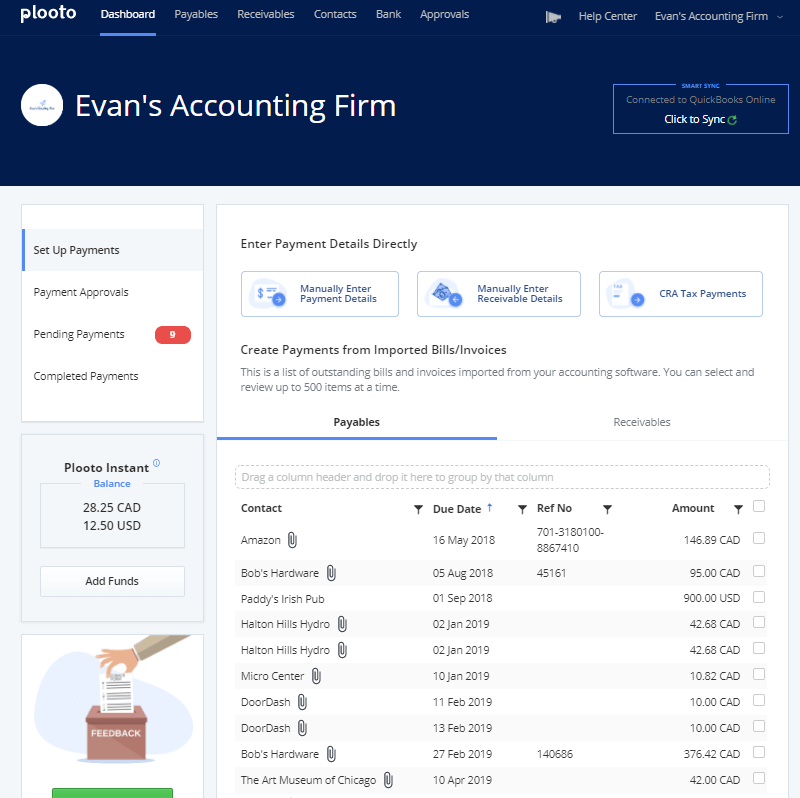

Once you have set up your suppliers, and started to enter your payables, you’ll start to see a good overview similar to this example Plooto dashboard:

You have to be a little bit patient

We’re used to Interac e-Transfers and wires that move funds quickly. However, in this case, both services take 3-4 business days to deposit the payment into the recipient’s bank account. This has more to do with banking regulations than Plooto or RBC PayEdge’s abilities. To expedite the process by a day or so, you can move funds ahead of time into a virtual wallet (that is, a pre-funded balance).

Record keeping

If there are any issues in the payment, or if the vendor can’t find it, records are easily accessible. If you have trouble, Plooto and RBC PayEdge could be more responsive in terms of customer service than a big bank.

Auto-schedule and deferral of payment

It’s possible to post-date a payment, or set up a regularly recurring payment, such as monthly rent.

Comparing Plooto and RBC PayEdge

Cost

At the moment, RBC PayEdge charges $1 per domestic payment (slightly higher for Canada Revenue Agency remittances). A foreign wire is $16. There are options for a flat monthly charge as well.

Plooto charges a monthly fee of $25 which covers 10 domestic transactions and one foreign payment. Starting with the 11th transaction, each domestic payment is $0.50.

Foreign exchange is competitive as well (that is, the fees are lower than a major bank), but it’s always good to check with your bank to see if you can get a better rate. You might still be better off using a service dedicated to foreign exchange and foreign payments, such as Wise (formerly TransferWise) or OFX.

You also have to consider any charges on your bank’s side. Payments made through RBC PayEdge and Plooto should be considered “pre-authorized transfers” that most banks don’t charge extra for, or are counted as standard transactions within your bank’s monthly plan limits.

Ownership

As mentioned above, RBC PayEdge is owned by RBC. This makes it an easier sell with clients. The downside is that it’s no longer a nimble startup. Fee structure and other functionality could change based the parent company’s goals.

Last I spoke with Plooto, it intended to remain independent.

What’s it like to “deal” with them

In general, I found both companies fairly easy to communicate with. I found Plooto to be quicker to respond, though.

In terms of integration and the various menus, Plooto wins. For example, accounting software integration is automatic in Plooto whereas RBC PayEdge requires that you click to “sync” and then wait. For foreign wires, Plooto requires less recipient information to be entered (i.e., foreign bank account information), whereas RBC PayEdge requires more (full foreign bank address, full foreign recipient address). RBC PayEdge data entry screens are also trickier in some cases.

Extras

RBC PayEdge does not at the moment have accounts receivable functionality. Plooto does. There are some factors to consider, including your relationship with your customers and getting pre-authorized payment agreements.

Conclusion

I am so glad I implemented one of the above systems for each of my clients. The pandemic has been tough and I can’t imagine what it would have been like if on top of everything we also had to deal with paper payments and cheques. The transition to working remotely has been quite seamless for all the clients who were willing to move to the cloud and adopt new technology.

I highly recommend that you try out the above solutions.

About the author

I am a Chartered Professional Accountant working somewhere in Canada. I provide controllership, training, and consulting services to small and medium sized businesses. I also work with non-profit organizations. I write only about my experiences in the business world and I am not selling or advertising any company or service, including my own. Audrey Silva is my pen name.

Facebook

Facebook Twitter

Twitter Email this

Email this