Over the last few years, a pesky term known as inflation has dominated media headlines and dinner table conversations. The culprit behind the rising costs of goods and weakening purchasing power, inflation continues to impact everyday folks. In fact, for 2025, the average Canadian household is on pace to spend $1,000 more per year just to buy the same basket of goods as two years ago. This increase is almost a 27% rise in 5 years for groceries alone or an annualized rise of 5.4%! While the Bank of Canada has worked to bring inflation down to a 2% target, the impact is still felt daily by savers, investors, and consumers. This pinch is altering everyday lives and is pushing people to new investment vehicles, income sources, and strategic thinking just to make ends meet.

Because of this, a critical question arises: “How does someone protect more of their money from inflation to get more cents for their dollar?”

High Interest Savings Accounts (HISAs) and Guaranteed Investment Certificates (GICs) offer different trade-offs between safety, accessibility (liquidity), and growth. But which option helps you stay afloat in today’s environment? Are there other safe alternatives? To determine which investment option is beneficial for an investor’s unique financial situation, they must first understand the basics of inflation and how it impacts returns and purchasing power.

Inflation: the basics

Inflation is the rate at which the price of goods and services rises over time. The result is the reduction or weakening in purchasing power for a consumer, as their money becomes less valuable. In other words, as inflation increases, your money buys fewer goods and services than it did before. Typically, inflation is measured by government agencies using the Consumer Price Index (CPI) or the Producer Price Index (PPI). Having limited to no inflation is often the target for most governments and central banks, but inflation can spike or change for various reasons, including:

- Demand-pull inflation: When the demand for goods and services exceeds supply, causing prices to rise (and in most cases never to decline back to their previous levels). This is sometimes referred to as excess spending, where the higher demand causes higher prices due to limited supply.

- Cost-push inflation: When the cost of production increases (for example, due to higher wages or increased costs of raw materials), leading to higher prices for consumers.

- Built-in inflation: Often referred to as a “wage-price spiral”, this occurs when workers demand higher wages to keep up with rising costs, which causes businesses to raise prices to cover the higher operating costs.

- Monetary inflation: When a government or central bank prints more money thereby increasing the supply, which causes a decrease in the currency’s purchasing power, often resulting in price increases. This is generally referred to as currency devaluation.

What is important to note is that inflation is generally seen as a natural part of the economic cycle, where it ebbs and flows (has high and low periods), but when it’s too high or too low, it can be problematic. That is why central banks, like the Federal Reserve in the U.S., or the Bank of Canada (BOC) try to manage it through monetary policies, such as interest rate adjustments and overnight lending rate changes, all with the goal of having a 2% inflation target.

Types of inflation

Like most things, there are various types of inflation. High inflation reduces the value of money, making it harder for consumers to afford basic goods. On the opposite side, deflation, or negative inflation, can lead to economic stagnation and higher unemployment. And then there is the beast with two backs: stagflation. Stagflation is a rare, but still occurring economic condition in which inflation is high, but there is negative economic growth and generally high unemployment.

| Feature |

High inflation

| Deflation |

Stagflation |

| Inflation |

High |

Negative |

High |

| Effect on money value |

Reduces the value of money |

Increases the value of money |

Reduces the value of money |

| Effect on consumer costs |

Harder for consumers to afford basic goods |

Consumers can buy more for less |

Harder for consumers to afford basic goods |

| Economic growth |

Growing, but often slowly |

Stagnating or declining |

Slow or negative growth (stagnation) |

| Unemployment |

Typically, low unemployment |

Higher unemployment |

High unemployment |

| Example |

2008 global financial crisis |

Great Depression (1930s) |

1970s oil crisis |

Inflation: The baseline you want to beat

In mid-2025, Canada’s headline inflation sat at 1.9%, slightly below the Bank of Canada’s target. That means for every $100 today, it will buy $98 worth of goods and services in a year. In other words, the everyday consumer is losing money by not investing it. As a result of the deprecation in purchasing power, any investment return should aim to beat inflation just to keep personal finances unchanged.

Luckily in the modern investment landscape, there are plenty of vehicles that can be leveraged, such as a High Interest Savings Accounts (HISA), Guaranteed Investment Certificates (GICs), and more!

High Interest Savings Accounts (HISAs)

HISAs are an extremely attractive investment vehicle for an investor to try and outperform inflation. This is because they are the most liquid investment option for an investor, and they come with little to no associated fees. As a result, investors can deposit money into a HISA, earn interest immediately, and withdraw the funds with ease. The drawback is that the interest rates are generally lower, ranging from 0.5% (or less) — typically offered by the Big Six Banks — up to around 3.0%, which are usually available through challenger banks and digital institutions. Currently, you can also get almost 5.0% through various short-term promotions. HISA rates are typically correlated with the Bank of Canada’s policy interest rates and the prime lending rate, but are not always adjusted at a direct proportion to the policy rate change. In addition to their liquidity and popularity, the average HISA (at least outside of one of the Big Banks) marginally outperforms inflation, providing little to no real growth, especially after taxes on the income earned. This is why most Canadians should consider rate shopping when it comes to their HISA, to ensure that their money is always working for them and compounding at the highest rate available.

For a competitive overview and for the highest rates and newest promotions in Canada that go beyond the Big Six Banks, investors can find more details and rates on the high interest savings comparison chart.

Guaranteed Investment Certificates (GICs)

GICs require you to lock in your money for a set term that is often linked to the overnight lending rate set by the Bank of Canada. In return for the reduced liquidity, you get a higher, guaranteed interest rate compared to a HISA. GICs work best for investors who want certainty, do not need immediate access to their funds, and prefer to see a more linear gain. Current rates can be found in more detail on the GIC rates comparison chart, but on average are between 3.40%-4.00% depending on the type, term, and payout instructions.

Compared to inflation, GIC returns generate modest growth, even after tax on the income earned. For example, a $1,000 one-year GIC at 3.6% would earn $36 before tax. Net of inflation, that is an extra $17 in purchasing power. While it does not sound like much, over time this growth and increase in purchasing power can add up.

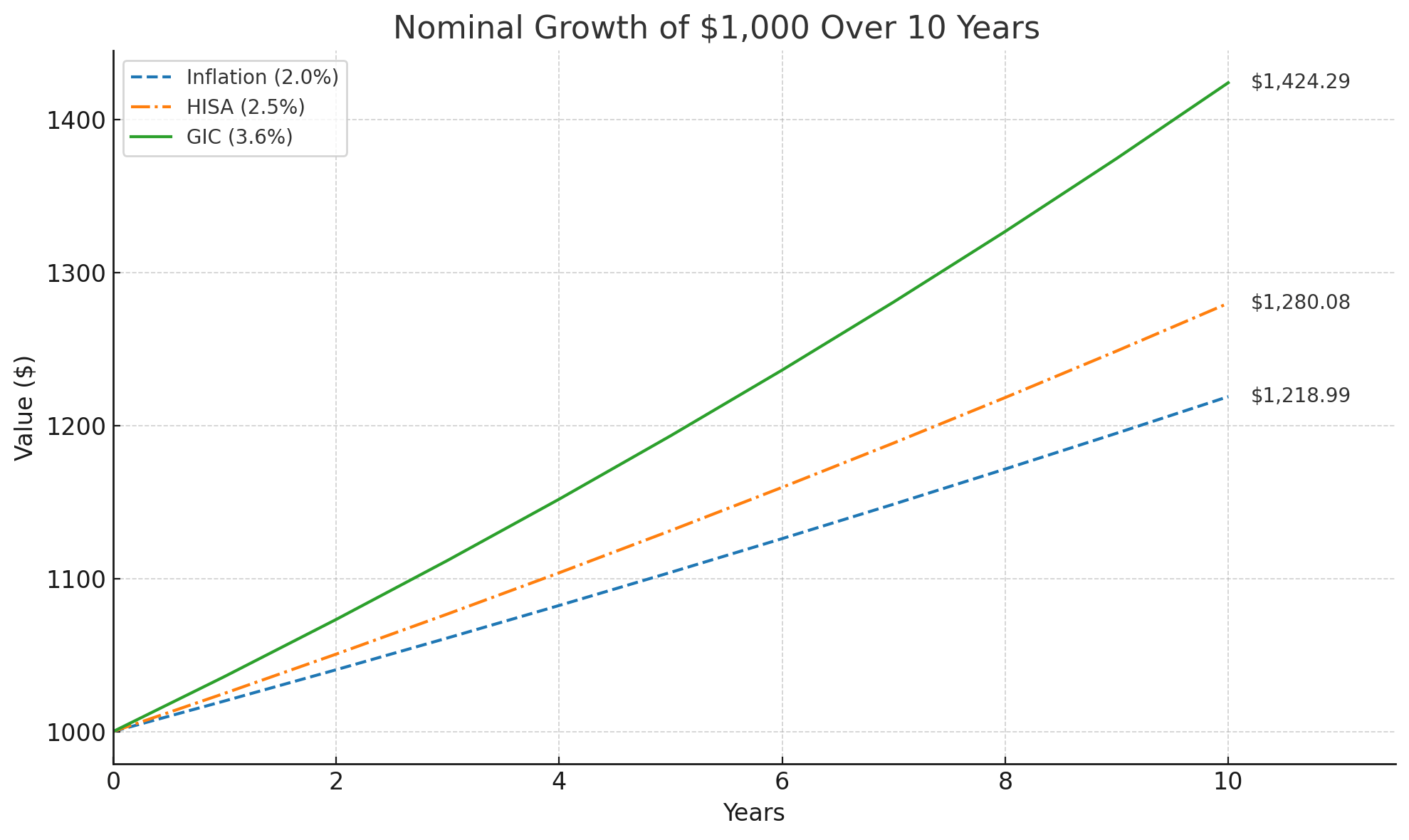

Head-to-head comparison: Inflation vs GICs vs HISAs

To better understand the growth and impact of inflation vs a GIC vs a HISA, we can track their returns. The following figure assumes that inflation has remained steady at a 2% target, a 1-year GIC with a simple annual interest is re-invested at 3.6% (based on recent historical averages) and a HISA from a challenger digital institution at 2.5%. The comparison is gross of taxes over a ten-year period and illustrates how the returns from a HISA are much smaller, despite the reality that in most years, a HISA results in marginal growth in purchasing power.

Nominal ending balances:

- Inflation (2.0%): $1,218.99

- HISA (2.5%): $1,280.08

- GIC (3.6%): $1,424.29

Inflation-adjusted (new purchasing power):

- Inflation baseline: $1,000 (by definition)

- HISA (2.5%) real value: $1,050.12

- GIC (3.6%) real value: $1,168.42

An equity alternative: index funds

For investors who have a longer-term outlook and can navigate higher volatility, there is the opportunity to invest in equities and alternative fixed income products through index funds or mutual funds. The S&P 500, for example, is an index of the 500 largest public companies in the US. Having historically returned ~10% per year (pending the fund), or about 6–7% after inflation, investors can see their purchasing power increase quicker. Over the past decade, returns have been even stronger, averaging over 9% after inflation. But as we know, past performance is not indicative of future returns.

Of course, the stock market fluctuates, so investors need to be aware of the risks. Some years can bring double-digit gains, while others bring losses. Unlike HISAs or GICs, there are no guarantees or capital preservation when it comes to traditional equity, index, and mutual fund investments. But over longer periods of time, their returns have consistently outperformed both inflation and fixed-income products, making them an appetizing growth tool.

The bottom line: balancing financial objectives to stay ahead

Inflation will continue to exist and be a part of our everyday lives. Being able to have an increase in purchasing power is ultimately a goal that most investors should have in the back of their mind so that they can continue to purchase goods and services, despite an increase in prices. As a result, the right investment choice depends on an investor’s goals, needs, and risk tolerance. In the modern investment world, it is not simply a choice between HISAs, GICs, or equities, but how to balance them in a way that keeps an investor’s money safe and ahead of inflation.

Disclaimer

This article is independently written and not sponsored by any financial institution. The views expressed are solely those of the author(s) based on their research and analysis. The content is for informational purposes only and should not be considered financial advice. Always consult a qualified financial professional before making investment decisions. Reading this article does not create a professional relationship with the author(s) or affiliated organizations. It is not a substitute for personalized financial guidance.

Investing involves risks, including potential loss of principal. Readers are solely responsible for their investment decisions. Past performance does not guarantee future results. Historical or projected returns may not reflect actual future performance. The use of information in this article is at the reader’s own risk. The author and publisher are not responsible for any errors, omissions, or resulting losses/damages.