EQ Bank joint accounts have been long-awaited and delayed at least a couple of times (from some time in 2019 and “end of” February 2020). As of June 25, 2020, EQ Bank joint accounts are finally here.

Setting up a joint account with EQ Bank is relatively straightforward and can be done completely online. Once you have an existing account, you can add someone to that account using the EQ Bank mobile app or your browser. Here’s how to do it in your browser.

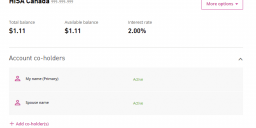

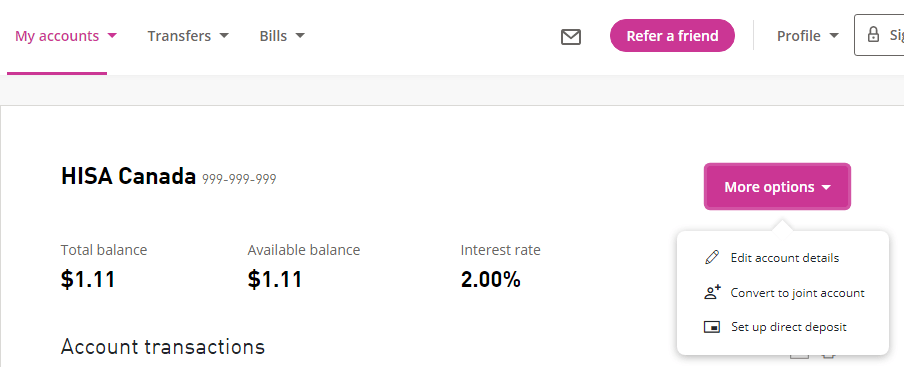

After you’ve logged in, browse to your account and then click the “More options” button. In the resulting dropdown menu, click the “Convert to joint account” link.

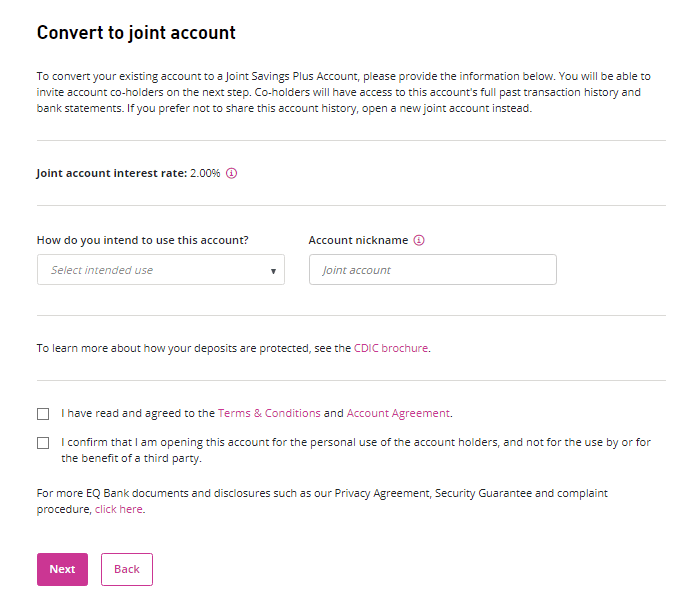

Then, complete the form for converting the account, which includes accepting the terms and conditions.

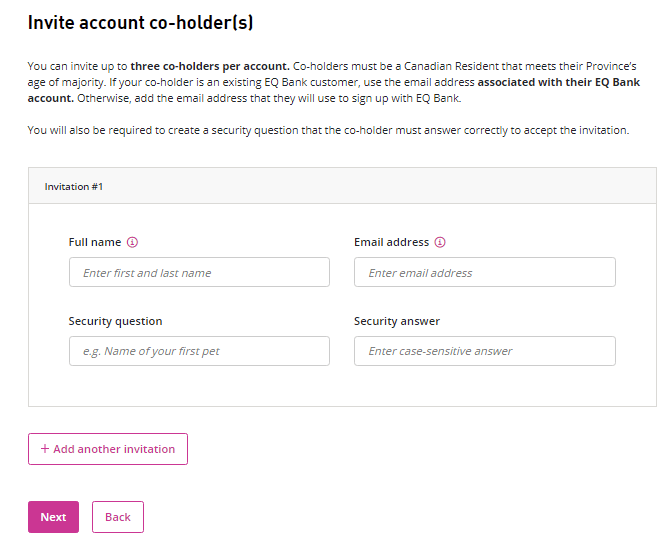

Next, add the account co-holder’s name and email address, and a temporary security question and answer that they’ll have to complete later.

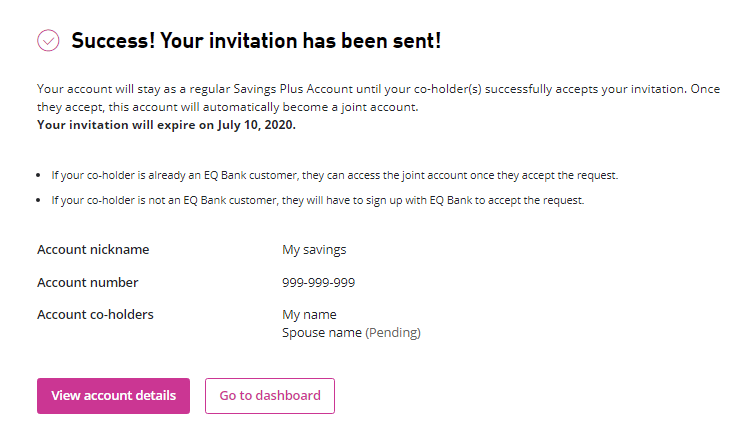

Your part is done. The confirmation page states that the co-holder will have 2 weeks to accept the invite:

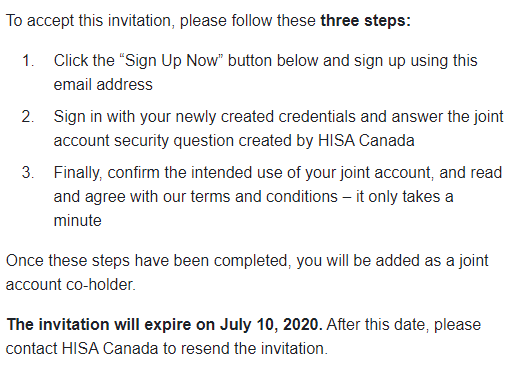

The desired account co-holder will then receive an invitation email with some general instructions on how to accept the invitation.

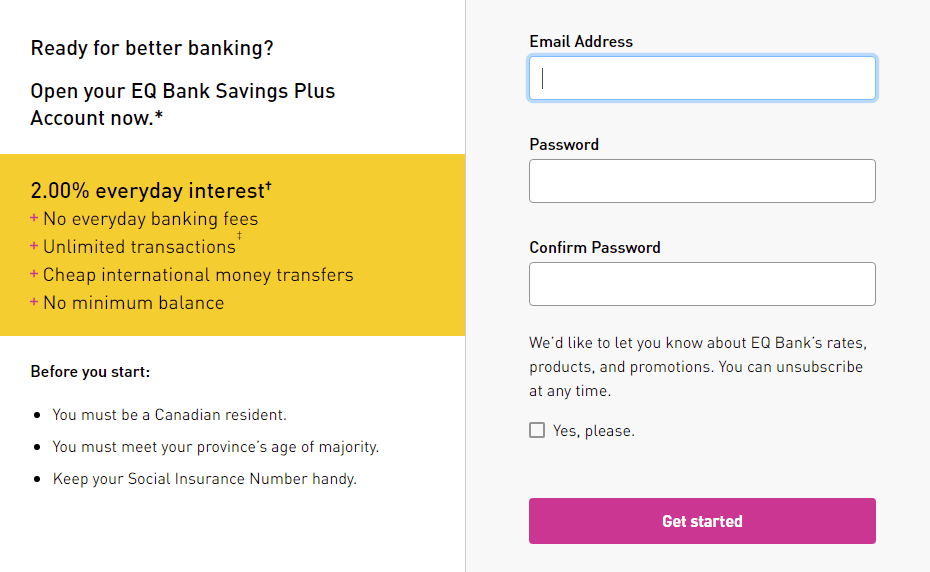

Once they click the link in the email, if they are already an EQ Bank customer, they can skip the next few steps and essentially log in and click a few buttons to complete the process. If they’re not yet an EQ Bank customer, the desired account co-holder will have to go through the account creation process, beginning by setting an email address to log in with, and a password.

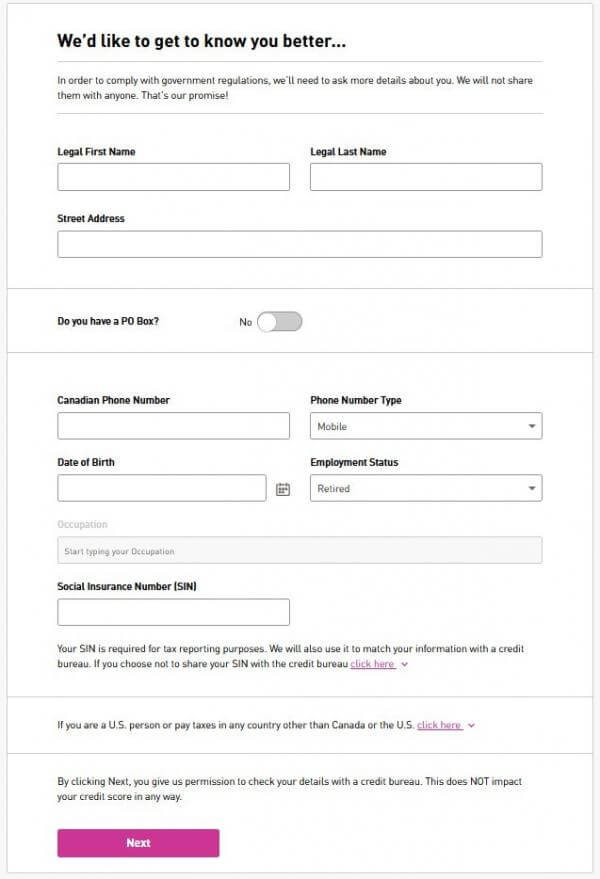

This will lead to a more complete sign-up form, where EQ Bank will collect their name and address, occupation information, Social Insurance Number, and more.

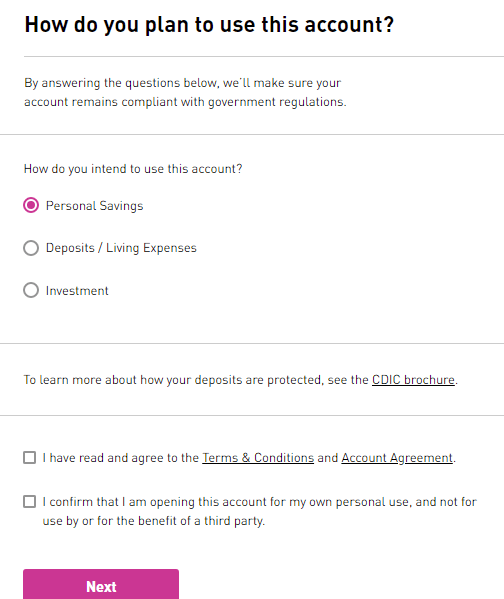

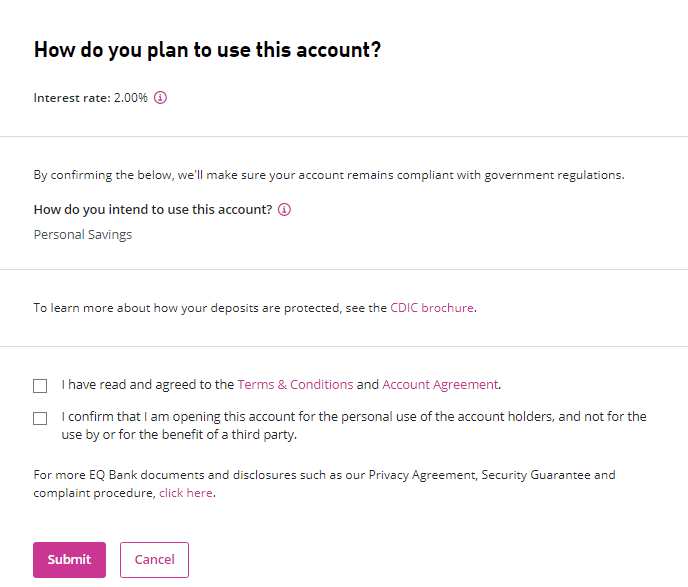

Next, the desired account co-holder must state the purpose of their account and agree to the terms and conditions.

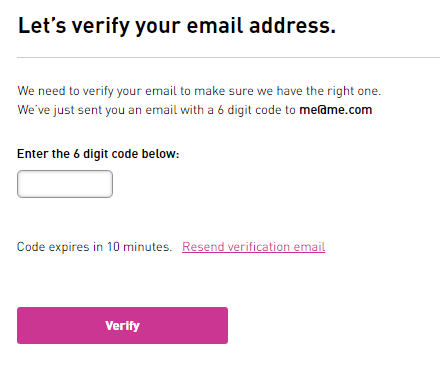

Lastly for the general account setup, they will have to enter a confirmation code sent to their email address.

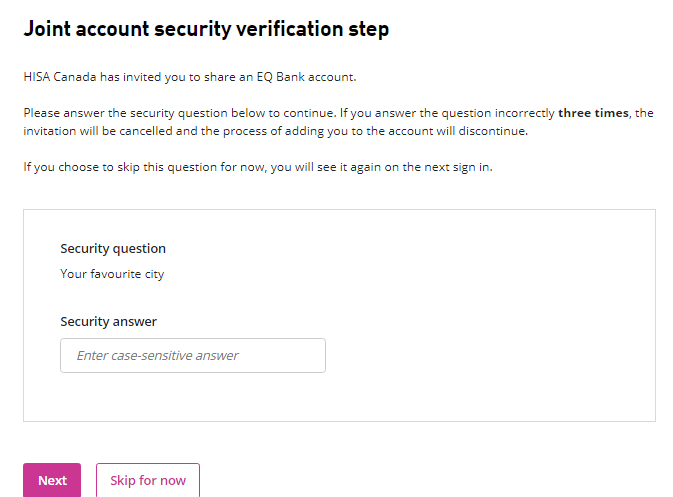

At this point, they can immediately complete the joint account setup by answering the security question you’d originally set up when sending the invite…

… and they must agree to the terms and conditions of the joint account.

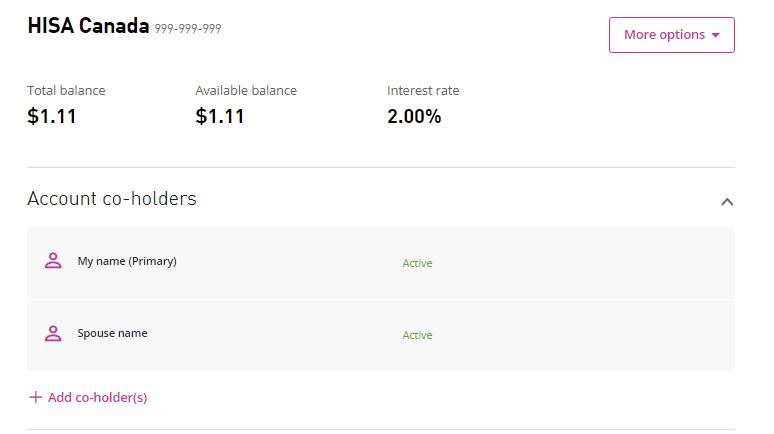

This process is complete, and you will both have access to the joint account!

Technically the account co-holder will now have at least 2 EQ Bank accounts, since their original account still exists. You as the original account holder and primary co-holder might still only have 1 EQ Bank account, since your original account was converted to a joint account.