Log In

Log In Register

Register

Topic RSS

Topic RSS

Facebook

Facebook Twitter

Twitter Email this

Email this11:08 am

February 20, 2018

Offline

Offline

Where to find? besides tangerine

11:14 am

February 27, 2018

Offline

Bud.

https://www.highinterestsaving.....gic-rates/

Touch on the "date" to see the gic history of the FI.

11:32 am

April 15, 2020

Offline

Bud said

Where to find? besides tangerine

I found the historical interest rates at Tangerine only recently. In the last 4-12 months. I was interested in a small segment of the information. They are competitive. I would expect the 5 year rates are within .25% of competition. I bought a short term deposit in May 2018. Then I tried longer term when I decided where I wanted to purchase. All rates can be adjusted anytime. For book keeping I prefer one statement. Each individual is UNIQUE.

1:17 pm

October 11, 2015

Offline

Does anyone want to look into their crystal ball and try to prognosticate where rates will go in the next few years? I'm thinking of purchasing a 2.2% Simplii GIC --I seemed to have missed the 2.5 and 2.8 rates!! Do we think this economic cataclysm with lost jobs and lost businesses will result in a low interest environment for years to come and I should purchase a 3 or 4 year GIC? Thank you. (I know that I should have laddered GICs, but most of mine will come due in the next year).

1:41 pm

December 12, 2009

Offline

dentgal said

Does anyone want to look into their crystal ball and try to prognosticate where rates will go in the next few years? I'm thinking of purchasing a 2.2% Simplii GIC --I seemed to have missed the 2.5 and 2.8 rates!! Do we think this economic cataclysm with lost jobs and lost businesses will result in a low interest environment for years to come and I should purchase a 3 or 4 year GIC? Thank you. (I know that I should have laddered GICs, but most of mine will come due in the next year).

Depends on your risk tolerance and whether you ever exceed your CDIC limits. If 'yes' to the latter, have a look at 1-10 year high investment grade corporate bonds ('A' or higher). Bank of Canada actions have helped to stabilize bond market by providing liquidity, but there were some decent 3-5% yields a few weeks ago. If 'yes' to both, then have a look at Canadian bank common shares. Unless you need to draw on the principal in a significant way, you will almost certainly be hugely rewarded for going that route.

If insisting on a GIC for comfort, then the Simplii GIC is as good as any, and you've got CIBC's very high investment grade deposit and bond ratings. Like I said, though, you may want to look into a CIBC corporate bond. The latter not guaranteed by CDIC, but is guaranteed by CIBC. So, unless you see one or more Big 5 banks going under, I'd go that route.

I do not see rates going higher in the next 5 years, at minimum. We will have sub-3.0% GIC rates for >= 5 years. As such, I've shifted my short-term bias to long-term in terms of GIC duration.

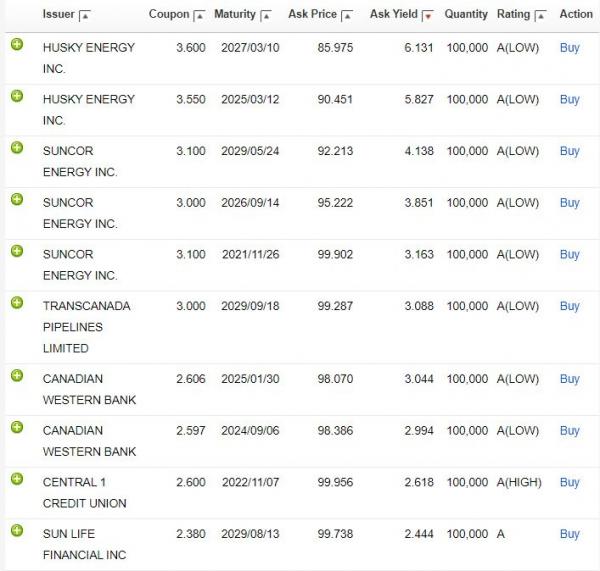

Edit: Including a fixed income screen screenshot from Scotia iTRADE. Parameters: below par, A-AAA (inclusive), and federal, provincial, municipal, and corporate. Much smaller list, but there's a Canadian Western Bank bond, below par, with a yield to maturity of > 3%. Also, Central 1 Credit Union has a similar bond. Central 1 is owned by the B.C. and Ontario credit unions.

Figure 1: 1-15 year corporate bonds rated A or higher from Scotia iTRADE as at today's date

Cheers,

Doug

4:54 am

October 11, 2015

Offline

Thank you, Doug. I do have a portfolio with Scotia MacLeod which includes lots of bank stocks, some preferred shares (which I never like), balanced funds, S&P 500, etc etc. I have always kept lots of CASH (as in GICs) as I was brought up by my Dad--who lived through the depression and always predicted another one. My dad--who was probably certifiably crazy--had a way of predicting things which seem to come true. Are we headed for another depression? He didn't invest at all. Only GICs. He would be rolling in his grave if he knew that I was so heavily invested. But I have about 1/2 of my portfolio in GICs--most are getting approx 3.0% and I can sleep at night. So the money that I was asking about is going to be re-invested in a GIC. So it sounds like you are suggesting a long term. (Right now, Simplii is paying me 2.8 until April 30th but I don't expect them to maintain this rate and I do think that things will slip down). Thank you again!

5:46 am

April 8, 2020

Offline

It all depends on the rate of inflation. There is a good argument inflation will be low for the next year or two ... three years at most. After that, my crystal ball doesn't give me much guidance.

I argue for shorter maturities, two years or three years tops. By that time, the stock market will have stabilized and dividend yields should be attractive. If inflation starts up, you'll be able to invest in higher yield GICs, or stocks that have some upside inflation protection.

7:43 am

February 27, 2018

Offline

Inflation is a very tricky beast. People and businesses want instant gratification.

"X" buys a company and the first thing they do is jack up the product price, in an effort to recover their purchase price as quickly as possible. Tim Hortons (3g capital), Ontario's 407 and everything dealing with Rogers and Bell Media are perfect examples.

So will prices go UP to recover covid loss? Will taxes go up to recover covid expense? Alberta oil dropped to $1 a barrel and yet the Ontario gas prices went UP.

Greed, self entitlement and maybe a shortage of supply are going to make things very expensive. It's called, cutting off one's nose to spite their face.

7:51 am

April 15, 2020

Offline

dentgal said

Thank you, Doug. I do have a portfolio with Scotia MacLeod which includes lots of bank stocks, some preferred shares (which I never like), balanced funds, S&P 500, etc etc. I have always kept lots of CASH (as in GICs) as I was brought up by my Dad--who lived through the depression and always predicted another one. My dad--who was probably certifiably crazy--had a way of predicting things which seem to come true. Are we headed for another depression? He didn't invest at all. Only GICs. He would be rolling in his grave if he knew that I was so heavily invested. But I have about 1/2 of my portfolio in GICs--most are getting approx 3.0% and I can sleep at night. So the money that I was asking about is going to be re-invested in a GIC. So it sounds like you are suggesting a long term. (Right now, Simplii is paying me 2.8 until April 30th but I don't expect them to maintain this rate and I do think that things will slip down). Thank you again!

My parents were brought up during the depression. I helped them invest some of their GICS in stocks.

3:18 pm

October 21, 2016

Offline

dentgal said

Does anyone want to look into their crystal ball and try to prognosticate where rates will go in the next few years? I'm thinking of purchasing a 2.2% Simplii GIC --I seemed to have missed the 2.5 and 2.8 rates!! Do we think this economic cataclysm with lost jobs and lost businesses will result in a low interest environment for years to come and I should purchase a 3 or 4 year GIC? Thank you. (I know that I should have laddered GICs, but most of mine will come due in the next year).

FWIW, two-thirds of my assets are currently invested in GIC at 3.1%, 3.2% and 3.25% all for 5 years. The 3.1% and 3.25% started around last July and the 3.2% is from Tang about a month ago.

If you look at the rates before covid-19 it might give you a bit of an idea of what might happen after covid-19. In summary I would say if you are a gambler go for 1 year and if you are a chicken go for 5.

I have another 6 figure GIC coming due in July and I'm thinking to go with one year to see what the situation will be by then. With two-thirds of my assets at an 'acceptable' rate for 5 years I can take that chance.

Knowing you had GIC coming due soon it is unfortunate you didn't borrow money for a few months in order to take advantage of Tang 3.2% for 5 years. I did that in addition to breaking a RRSP GIC (and lose the accumulated interest) in order to take advantage of the 3.2%. I also invested a 6 figure at 3.2%.